Naked Bimodal Peak Condor Spread

This strategy represents an adaptation of the previously discussed Bimodal Peak Condor Spread where instead of limited risk, we have unlimited risk and a better reward.

The easiest way to achieve a similar payoff graph to the Bimodal Peak Condor is by omitting the purchases of the farthest out-of-the-money (OTM) call and put options.

However, there’s an alternative method to construct a strategy with a comparable payoff structure:

A Call Ratio Front Spread where you utilize different strikes for the distant OTM calls + A Put Ratio Front Spread, also employing different strikes for the distant OTM puts.

This configuration maintains the twin-peak profit structure, similar to what we see in the Bimodal Peak Condor Spread, while potentially offering a different risk-reward balance tailored to specific market expectations.

Let’s look at both of the parts separately before we combine them.

Put Ratio Front Spread with Different Strikes for Distant OTM Puts:

- If the sold distant OTM put are at different strikes, it’s still essentially a Put Ratio Front Spread.

- This variation adds a layer of complexity to the strategy. The different strike prices can be chosen to fine-tune the risk and reward profile based on specific market expectations.

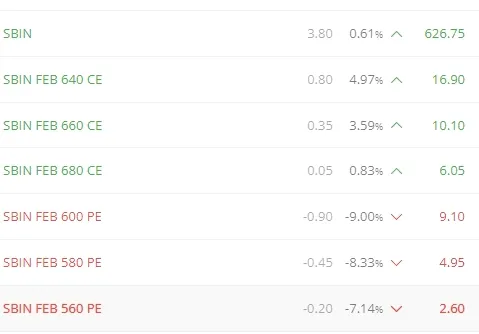

Example –

When we similarly construct strangles instead of straddles to what we have done for Ratio Spread we get the following –

- Buy 640PE at 9.1 – 1 Lot

- Short 580PE at 4.95 – 1 Lot

- Short 560PE at 2.60 – 1 Lot

Call Ratio Front Spread with Different Strikes for Distant OTM Calls:

- If the sold distant OTM calls are at different strikes, it’s still essentially a Call Ratio Front Spread.

- This variation adds a layer of complexity to the strategy. The different strike prices can be chosen to fine-tune the risk and reward profile based on specific market expectations.

Example –

When we similarly construct strangles instead of straddles as we have done for Ratio Spread we get the following –

- Buy 640CE at 16.9 – 1 Lot

- Short 660CE at 10.1 – 1 Lot

- Short 680CE at 6.05 – 1 Lot

Payoff Graphs

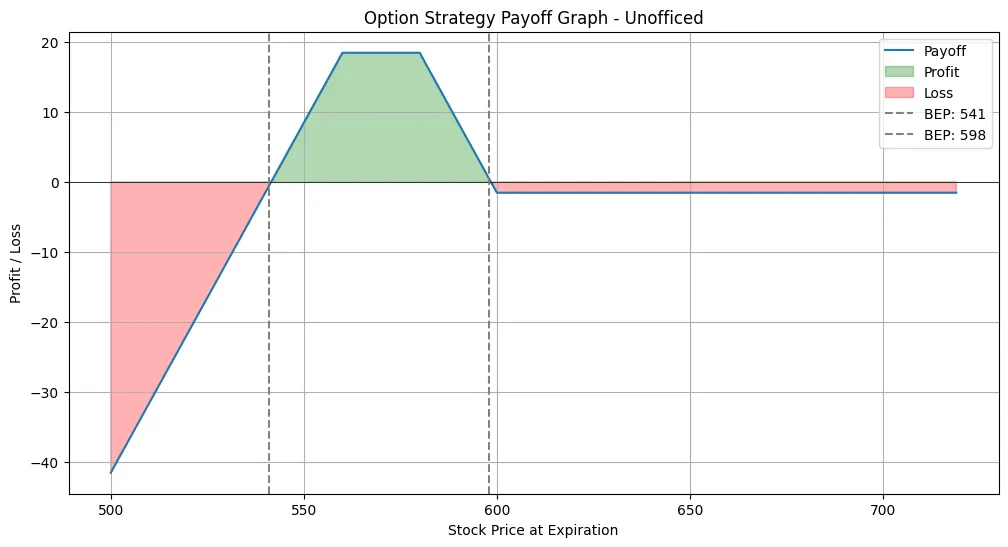

The payoff graph for the Put Ratio Front Spread with Different Strikes for Distant OTM Puts looks like this –

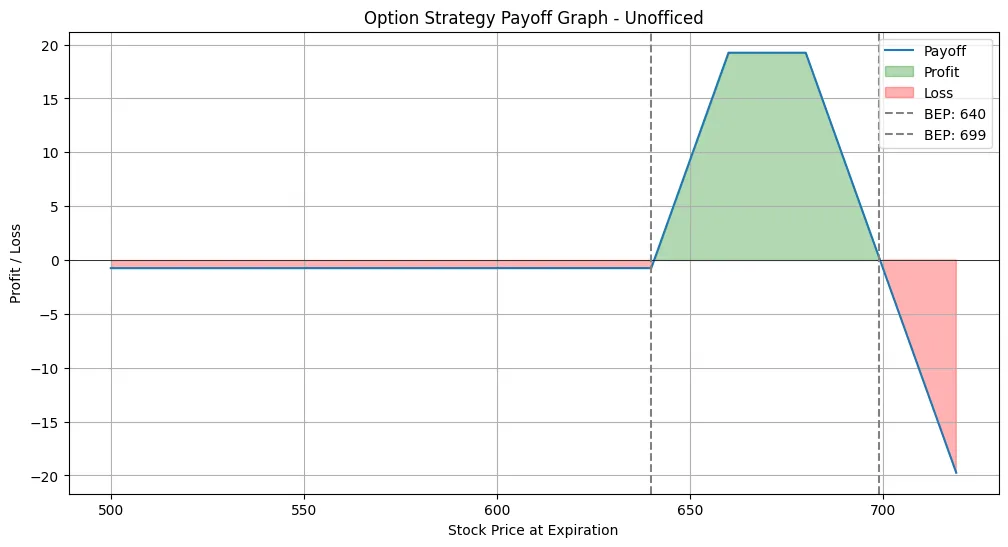

The payoff graph for the Call Ratio Front Spread with Different Strikes for Distant OTM Calls looks like this –

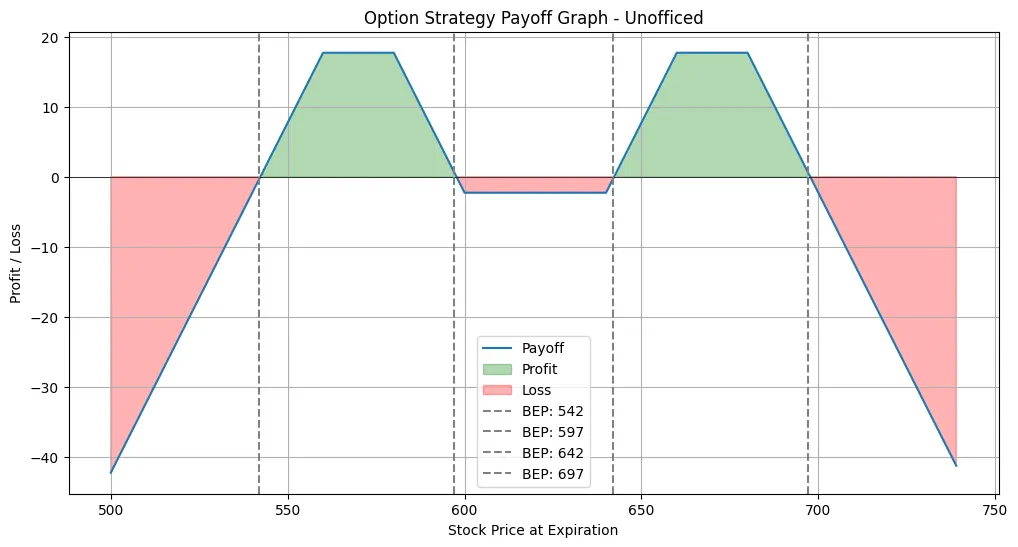

Now, If we combine them, We get –

This exactly looks like Bimodal Peak Condor Spread but it has a higher risk (unlimited) but also has a higher reward.