Options Premium Calculator using Black Scholes Model: Google Sheet

Call option C and put option P prices are calculated using the following formulas:

![]()

![]()

where N(x) is the standard normal cumulative distribution function.

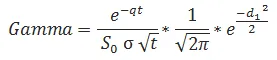

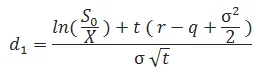

The formulas for d1 and d2 are:

![]()

![]()

![]()

… where T is the number of days per year (calendar or trading days, depending on what you are using).