The Black 76 Option Pricing Model

If you see any single guy who is using Black Scholes Model, ask him how he handles the cases when “futures” price trade-in discount because that will result in a crisis.

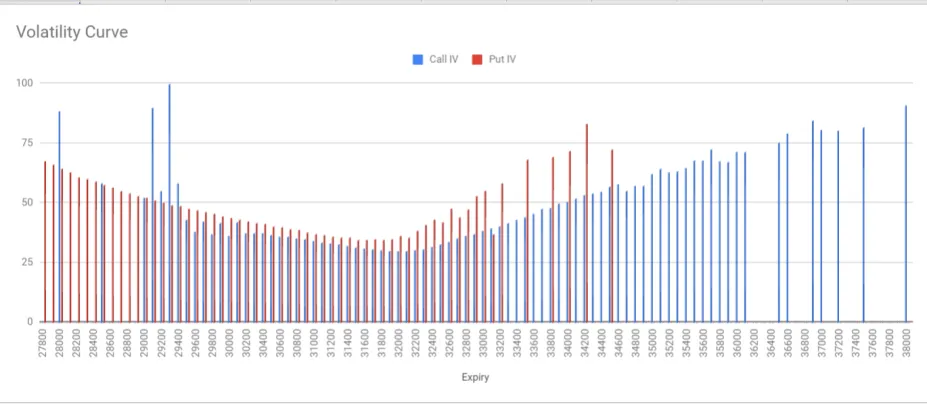

IV Calculation is what is which is interesting.

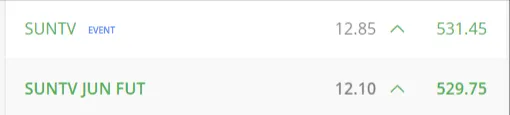

The way the NSE website throws the IV is calculated from the proper Black Scholes Model with their own twist (because the data never matches). If You go to “Option Chain” of any stock or index in NSE India website, You can see –

Black Scholes Options Pricing Model assumes that risk-free rate and volatility of the underlying are known and constant.

Black 76 Models reverse calculate the IV.

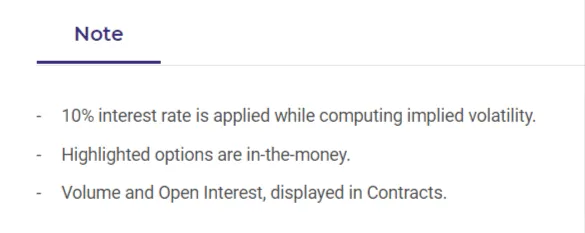

NSE assumes an interest rate of 10% all the time. So, right now, if someone is telling that he is using the NSE site’s IV in his professional quant models, he is not a professional.

*Not talking about Price Action Traders. Pure Quants.

** Actual Calculation should take RBI’s Interest value each day which will result in a massive difference.

There are arbitrage strategies often playable by higher AUM in events of RBI Interest Rate.

Now tell,

If RBI slashes interest rates, then –> Put prices will _____ and Call prices will ____

In reality, interest rates usually change only in increments of 0.25%. or decrements of 0.25%. I did some further calculations. When RBI increments or decrements interest by 0.25% the change in call put prices is about 6 INR. [Suppose BN is trading at 30000. 30000PE is trading at 100. The lot size is 25. So, change will be like 100.24 which is meh as you lose more than that in Slippage which tells discussing that without being trillionaire is baseless.]

You can read more about Rho here –

It is one of such theories like when Ashoka invaded Kalinga. You don’t know what to do with that information at the later stage of your life.

At this moment –

- There are two libs. One is Mbian.

- Another I used in my first day for JS for my some startup is this gist by some good guy . Check here and You can tweak as per your will!