Backtesting MACD Crossover Strategy in Multiple Instruments

In the previous chapter, we conducted numerous backtests on NIFTY Futures. Now, let’s venture into analyzing the MACD Crossover Strategy across a variety of other instruments to unravel its underlying mechanics.

As we broaden our horizon beyond NIFTY, it opens up an avenue to compare and contrast how the strategy holds up across different market conditions and instruments. Whether it’s equities, commodities, or forex, understanding the adaptability and effectiveness of the MACD Crossover Strategy is crucial. This endeavor will not only provide a holistic view of its performance but also enrich our strategic toolkit.

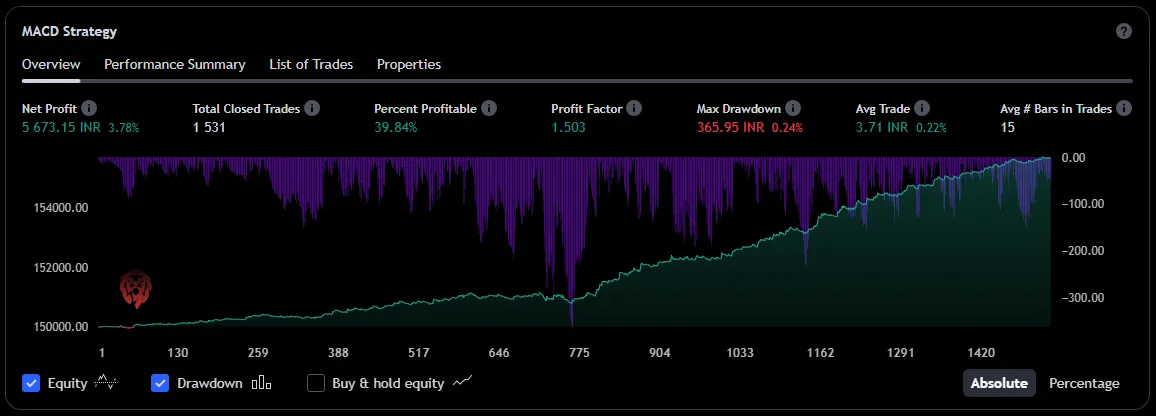

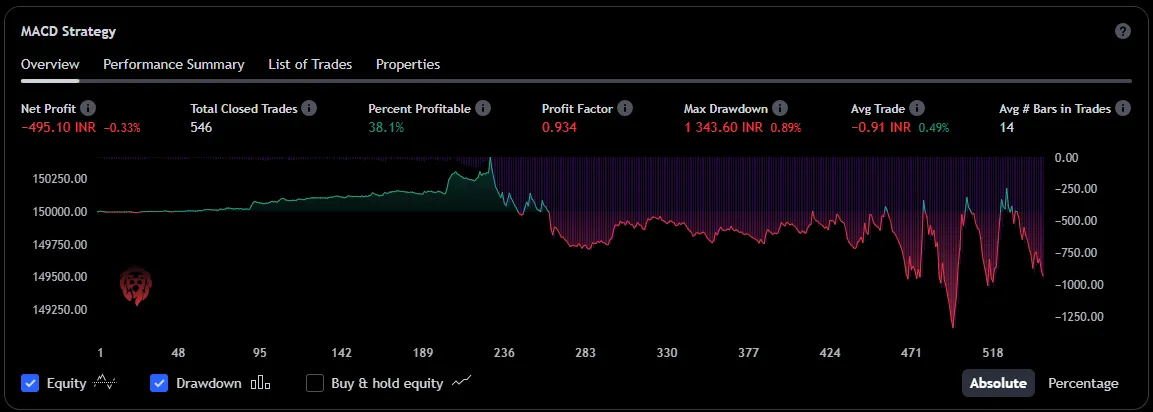

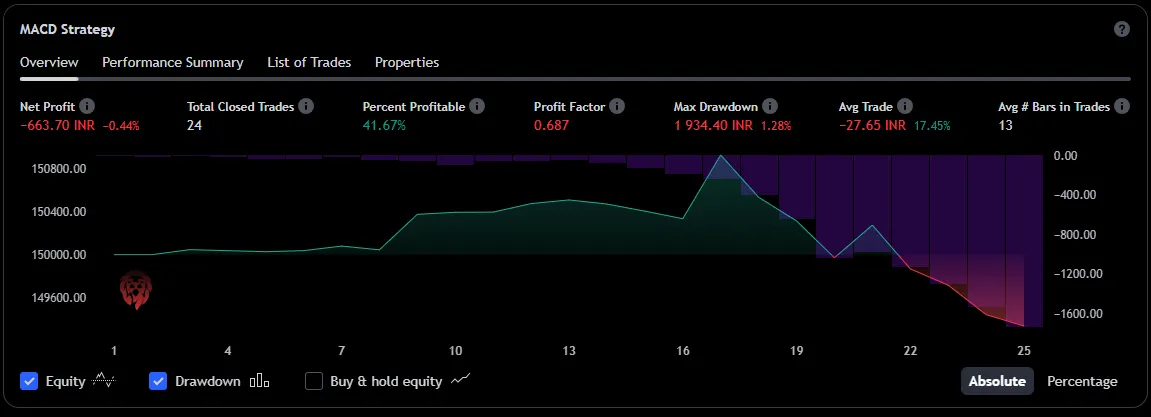

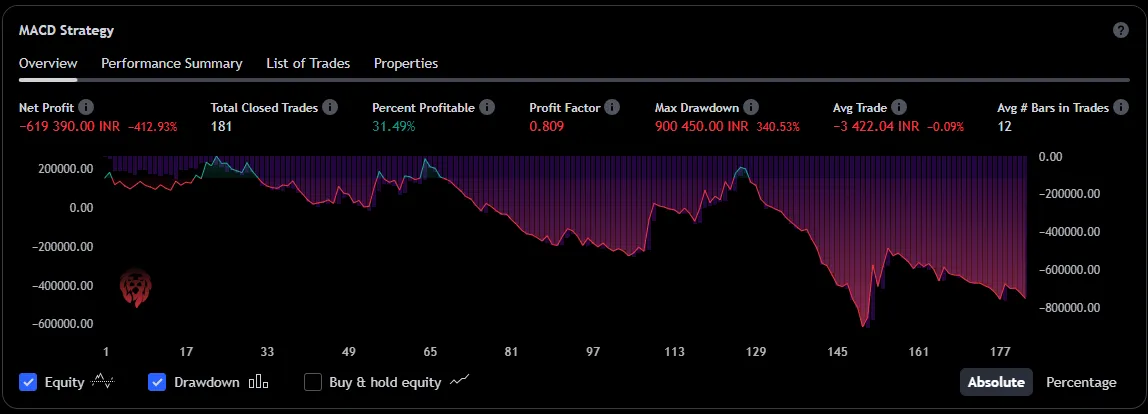

Backtesting Reliance Equity

In this section, we are conducting backtests on Reliance Equity with a capital of 1000 INR with 1 quantity. Although it would have been easier to visualize if you just did with x amount of quanity but that will come distorted because of coporate results like stock split and bonus etc.

15 Minutes Timeframe

30 Minutes Timeframe

1 Hour Timeframe

1 Day Timeframe

1 Week Timeframe

1 Month Timeframe

It’s quite intriguing to observe that, Reliance incurred substantial losses in most of the timeframes and made minor profits in smaller timeframes. Moreover, in many cases the drawdown is more than the profit itself!

- Now, what about stocks that exhibit cyclical behavior?

- Could the MACD have a different impact on such stocks?

This opens up an avenue for further examination to understand the behavior of cyclic stocks in relation to the MACD Crossover strategy.

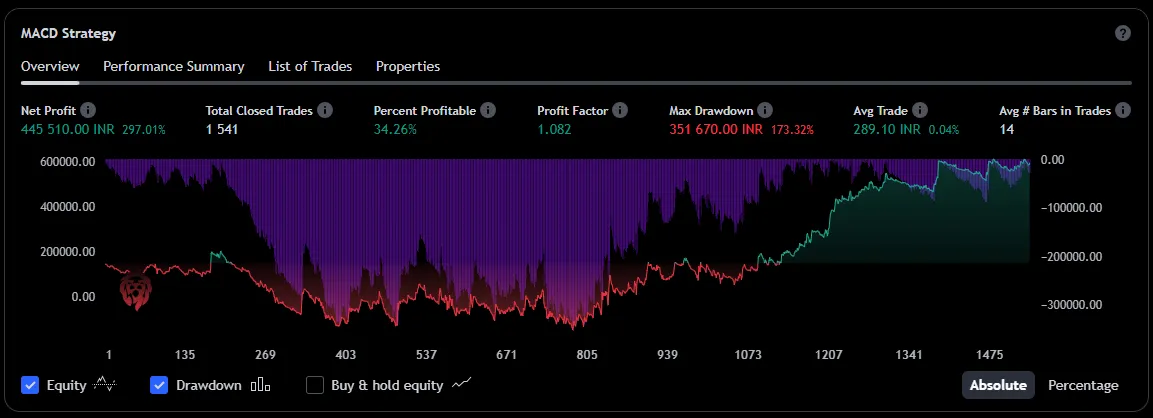

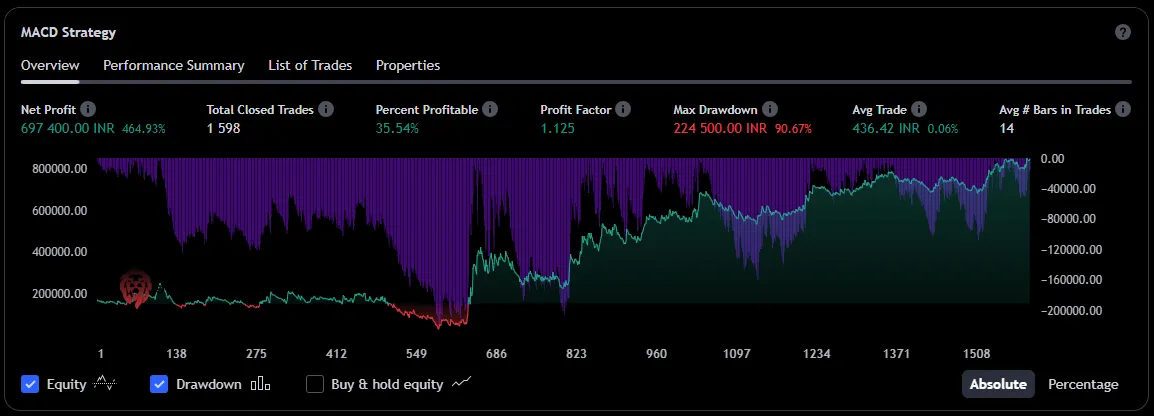

Backtesting Vedanta Futures

In this segment, we will shift our focus towards conducting a similar backtest on Vedanta stock, a commodity-based entity known for its cyclic nature. The cyclicality in commodity-based stocks often mirrors the fluctuations in commodity prices, thereby presenting a distinct pattern of price movements over time.

This characteristic trait of Vedanta prompts an intriguing inquiry: how would the MACD Crossover strategy fare when applied to a commodity-centric, cyclic stock? Will the outcomes deviate from what we observed with Reliance, or align more with the patterns seen in the index?

15 Minutes Timeframe

30 Minutes Timeframe

1 Hour Timeframe

1 Day Timeframe

1 Week Timeframe

1 Month Timeframe

In line with our anticipation, the strategy showed a robust profitability compared to Reliance when applied to Vedanta across the majority of timeframes.

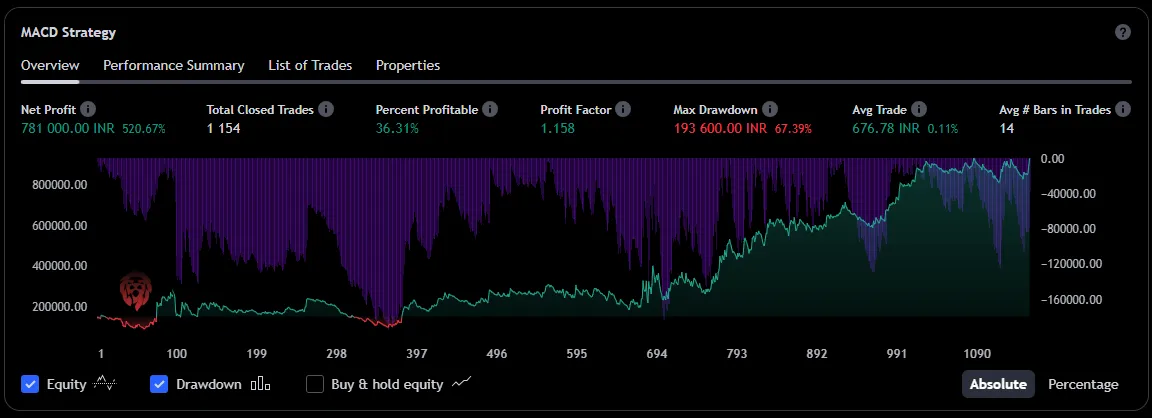

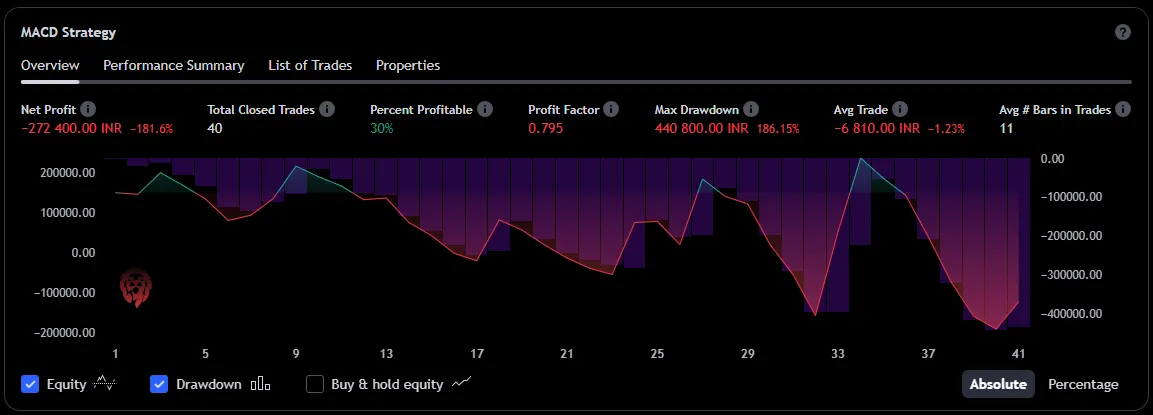

Backtesting Crude Oil Futures

Now, What if it is applied to Crude Oil directly. It is a commodity. It is cyclic in nature.

15 Minutes Timeframe

30 Minutes Timeframe

1 Hour Timeframe

1 Day Timeframe

1 Week Timeframe

1 Month Timeframe

The MACD Crossover strategy applied in 1 hour timeframe in the Crudeoil is the best strategy so far!

Although the higher timeframe, we have encountered loss but the number of trades in the higher timeframe is too less to be considered as a deal breaker!

Backtesting != Future Performance

However, it’s pivotal to retain a cautious perspective, as backtesting results are not definitive indicators of future performance. Here are some key points to consider:

Historical Performance vs Future Outcomes: Backtesting operates on historical data; it doesn’t account for potential future market changes. The past performance of a strategy does not guarantee similar outcomes in the future.

Market Conditions: Market conditions are in a constant state of flux, influenced by numerous external factors such as economic events, policy changes, and global occurrences. These factors can significantly impact a strategy’s effectiveness.

Overfitting: There’s a risk of overfitting when a strategy performs exceptionally well on past data. It might be tailored to past conditions and may not adapt well to new, unforeseen market scenarios.

Brokerage Fees and Slippage: Backtesting often overlooks the real-world implications of brokerage fees and slippage which can considerably affect net profitability.

Data Snooping Bias: Repeated backtesting across numerous instruments and timeframes can lead to data snooping bias, where a strategy might appear more effective than it genuinely is due to chance.

Well Overfitting is exactly what currently we are doing right now. We are basically looking for the timeframes it performed exceptionally well. Isn’t it?

Anyways, Engagement with different market instruments and exploring various timeframes can be an enriching exercise. It not only broadens your understanding but also enables a more comprehensive evaluation of the strategy’s versatility and robustness.