Backtesting Index Inside Bar Intraday Strategy Using Python

Let’s start by importing index_ib.csv file which was shared in the earlier chapter. It contains all dates when NIFTY and BankNIFTY Index exhibited Inside Bar Pattern since 2015 to today.

In case You have went through course of Coding Time Compression Scanners that shows how to scan the stocks for these bars from stratch, Please save the database to the same format and if needed add fake column entry to adjust with following tutorial –

Initialize the Database

df = pd.read_csv("/root/apps/trident/index_ib.csv")

df

The output will be –

date symbol marketcapname sector

0 01-12-2015 NIFTYFINSERVICE Smallcap Indices

1 01-12-2015 BANKNIFTY Smallcap Indices

2 07-12-2015 NIFTYFINSERVICE Smallcap Indices

3 10-12-2015 NIFTY Smallcap Indices

4 10-12-2015 NIFTYFINSERVICE Smallcap Indices

... ... ... ... ...

558 31-07-2023 BANKNIFTY Smallcap Indices

559 04-08-2023 NIFTYFINSERVICE Smallcap Indices

560 07-08-2023 BANKNIFTY Smallcap Indices

561 10-08-2023 NIFTY Smallcap Indices

562 17-08-2023 NIFTY Smallcap Indices

563 rows × 4 columns

Note that the uploaded files are sometimes updated with new files with current data. So, You may see slightly different format or more amount of data. Nothing to worry about.

Get Yesterday's High and Low and Today's Open Price

Next, we will cycle through each row of this Pandas database, applying our previously developed get_stock_data() function from the previous chapter. This function will provide us with three outputs:

- Yesterday’s high

- Yesterday’s low

- Today’s open.

We will then store these values in new columns.

import datetime

for index, row in df.iterrows():

symbol = row['symbol']

time = row['date']

high,low,today_open= get_stock_data(symbol, time)

df.at[index, 'high'] = high

df.at[index, 'low'] = low

df.at[index, 'today_open'] = today_open

df

The output looks like –

date symbol marketcapname sector high low today_open

0 01-12-2015 NIFTYFINSERVICE Smallcap Indices 0.00 0.00 0.00

1 01-12-2015 BANKNIFTY Smallcap Indices 17495.45 17353.85 17457.15

2 07-12-2015 NIFTYFINSERVICE Smallcap Indices 0.00 0.00 0.00

3 10-12-2015 NIFTY Smallcap Indices 7691.95 7610.00 7699.60

4 10-12-2015 NIFTYFINSERVICE Smallcap Indices 0.00 0.00 0.00

... ... ... ... ... ... ... ...

558 31-07-2023 BANKNIFTY Smallcap Indices 45694.90 45359.75 45740.00

559 04-08-2023 NIFTYFINSERVICE Smallcap Indices 0.00 0.00 0.00

560 07-08-2023 BANKNIFTY Smallcap Indices 45011.35 44773.85 44888.95

561 10-08-2023 NIFTY Smallcap Indices 19623.60 19495.40 19554.25

562 17-08-2023 NIFTY Smallcap Indices 19461.55 19326.25 19301.75

563 rows × 7 columns

Now there are some rows with `high` variable’s value as 0. Like Nifty Fin Service did not had futures data because it was not even in derivatives back then. Right? Let’s remove it.

# Remove rows with high value of 0

df = df[df['high'] != 0]

Checking the Condition of Gap Trigger

Also Check for the Condition of Gap Triggers

In case of gap up above the previous day’s high or gap down below the previous day’s low, please avoid buying it or selling it respectively. It means –

- If there’s a gap up above the previous day’s high (the sell point), it implies that the sell trade has already been triggered, so we avoid this scenario.

- Likewise, in the case of a gap down, we steer clear of situations where there’s a gap down below the previous day’s low (the buy point).

# Create 'gap_df' DataFrame containing rows with 'gap_trigger' as True

gap_df = df[df['gap_trigger']]

# Remove rows with 'gap_trigger' as True from the main df

df = df[df['gap_trigger'] == False]

# Reset index of both DataFrames

df.reset_index(drop=True, inplace=True)

gap_df.reset_index(drop=True, inplace=True)

print("Main DataFrame (df):")

df

The output looks –

date symbol marketcapname sector high low today_open gap_trigger

0 01-12-2015 BANKNIFTY Smallcap Indices 17495.45 17353.85 17457.15 False

1 31-12-2015 BANKNIFTY Smallcap Indices 16972.25 16896.65 16932.50 False

2 21-01-2016 NIFTY Smallcap Indices 7398.70 7250.00 7355.70 False

3 21-01-2016 BANKNIFTY Smallcap Indices 15364.60 14918.15 15343.15 False

4 15-03-2016 BANKNIFTY Smallcap Indices 15386.85 15268.10 15304.35 False

... ... ... ... ... ... ... ... ...

166 05-07-2023 NIFTY Smallcap Indices 19421.60 19339.60 19385.70 False

167 10-07-2023 NIFTY Smallcap Indices 19435.85 19327.10 19427.10 False

168 19-07-2023 BANKNIFTY Smallcap Indices 45707.40 45433.00 45689.05 False

169 07-08-2023 BANKNIFTY Smallcap Indices 45011.35 44773.85 44888.95 False

170 10-08-2023 NIFTY Smallcap Indices 19623.60 19495.40 19554.25 False

171 rows × 8 columns

gap_df database.

print(gap_df)

The output looks –

date symbol marketcapname sector high low today_open gap_trigger

0 10-12-2015 NIFTY Smallcap Indices 7691.95 7610.00 7699.60 True

1 23-12-2015 BANKNIFTY Smallcap Indices 16913.15 16812.50 16926.95 True

2 19-01-2016 NIFTY Smallcap Indices 7462.75 7364.15 7357.00 True

3 08-03-2016 BANKNIFTY Smallcap Indices 15326.65 15066.50 15022.35 True

4 29-03-2016 BANKNIFTY Smallcap Indices 15774.10 15580.80 15829.60 True

... ... ... ... ... ... ... ... ...

106 26-06-2023 BANKNIFTY Smallcap Indices 43773.10 43541.75 43804.55 True

107 05-07-2023 BANKNIFTY Smallcap Indices 45418.90 45073.40 45060.55 True

108 26-07-2023 BANKNIFTY Smallcap Indices 46096.60 45804.70 46285.85 True

109 31-07-2023 BANKNIFTY Smallcap Indices 45694.90 45359.75 45740.00 True

110 17-08-2023 NIFTY Smallcap Indices 19461.55 19326.25 19301.75 True

111 rows × 8 columns

That’s something to think about. Almost half the entries are gap triggers which is kind of considerable amount of dataset. You may explore other kind of strategies like Opening Range Breakout on those scrips.

But that is out of the purview of the current discussion. Anyways, let’s remove the gap_trigger, marketcapname, and sector columns because they are not needed.

# Remove columns 'gap_trigger', 'marketcapname', and 'sector'

df.drop(['gap_trigger', 'marketcapname', 'sector'], axis=1, inplace=True)

That’s something to think about. Almost half the entries are gap triggers which is kind of considerable amount of dataset. You may explore other kind of strategies like Opening Range Breakout on those scrips.

But that is out of the purview of the current discussion. Anyways, let’s remove the gap_trigger, marketcapname, and sector columns because they are not needed.

Setting the Target

This strategy already incorporates a built-in trigger and stop-loss mechanism. Here’s a concise explanation which we have already discussed earlier:

The stock’s high price plays a dual role:

- It acts as the stop-loss level when executing a sell trade.

- It serves as the trigger point to initiate a buy trade.

Similarly, the low price of the stock has its significance:

- It functions as the stop-loss level for buy trades once the buy order is placed.

- It serves as the trigger point for entering a sell trade.

In summary:

- High of the stock = Buy Trigger = Sell Stoploss

- Low of the stock = Sell Trigger = Buy Stoploss

Since this strategy inherently determines entry and stop-loss levels from the candlesticks, let’s now focus on defining profit targets. We’ll set the risk-reward ratio at 1:3 as a starting point.

Feel free to experiment with different risk-reward ratios, such as 1:5 or others, to further explore the strategy’s dynamics.

# Calculate and add buy_target and sell_target columns

df['buy_target'] = df['today_open'] + 3 * (df['high'] - df['low'])

df['sell_target'] = df['today_open'] - 3 * (df['high'] - df['low'])

df

The output looks like –

date symbol high low today_open buy_target sell_target

0 01-12-2015 BANKNIFTY 17495.45 17353.85 17457.15 17881.95 17032.35

1 31-12-2015 BANKNIFTY 16972.25 16896.65 16932.50 17159.30 16705.70

2 21-01-2016 NIFTY 7398.70 7250.00 7355.70 7801.80 6909.60

3 21-01-2016 BANKNIFTY 15364.60 14918.15 15343.15 16682.50 14003.80

4 15-03-2016 BANKNIFTY 15386.85 15268.10 15304.35 15660.60 14948.10

... ... ... ... ... ... ... ...

166 05-07-2023 NIFTY 19421.60 19339.60 19385.70 19631.70 19139.70

167 10-07-2023 NIFTY 19435.85 19327.10 19427.10 19753.35 19100.85

168 19-07-2023 BANKNIFTY 45707.40 45433.00 45689.05 46512.25 44865.85

169 07-08-2023 BANKNIFTY 45011.35 44773.85 44888.95 45601.45 44176.45

170 10-08-2023 NIFTY 19623.60 19495.40 19554.25 19938.85 19169.65

171 rows × 7 columns

Run The Buddha Backtester Function

Now that We have the following variables,

symbol: The stock symbol (e.g., “RELIANCE”).time: A time parameter (currently unused within the function).high: The stock’s high price.low: The stock’s low price.buy_target: The buy target price.sell_target: The sell target price.

Let’s run the check_high_breakout_and_save function we designed in our earlier chapter. This Python function is designed to scan historical stock price data and assess whether buy and sell trades are triggered, monitor trade targets and stop losses, calculate profits and losses, and manage trade exits.

import datetime

from pprint import pprint

# Iterate through the DataFrame and update 'entry_time' column

for index, row in df.iterrows():

symbol = row['symbol']

time = row['date']

high = row['high']

low = row['low']

buy_target = row['buy_target']

sell_target = row['sell_target']

buy_trigger,sell_trigger,buy_trigger_stoploss,sell_trigger_stoploss,buy_exit_time,buy_exit_price,sell_exit_time,sell_exit_price,buy_trigger_target,sell_trigger_target,buy_pl_points,sell_pl_points = check_high_breakout_and_save(symbol, time,high,low,buy_target,sell_target)

df.at[index, 'buy_trigger'] = buy_trigger

df.at[index, 'sell_trigger'] = sell_trigger

df.at[index, 'buy_trigger_stoploss'] = buy_trigger_stoploss

df.at[index, 'sell_trigger_stoploss'] = sell_trigger_stoploss

df.at[index, 'buy_exit_time'] = buy_exit_time

df.at[index, 'buy_exit_price'] = buy_exit_price

df.at[index, 'sell_exit_time'] = sell_exit_time

df.at[index, 'sell_exit_price'] = sell_exit_price

df.at[index, 'buy_trigger_target'] = buy_trigger_target

df.at[index, 'sell_trigger_target'] = sell_trigger_target

df.at[index, 'buy_pl_points'] = buy_pl_points

df.at[index, 'sell_pl_points'] = sell_pl_points

df

The output looks like –

date symbol high low today_open buy_target sell_target buy_trigger sell_trigger buy_trigger_stoploss sell_trigger_stoploss buy_exit_time buy_exit_price sell_exit_time sell_exit_price buy_trigger_target sell_trigger_target buy_pl_points sell_pl_points

0 01-12-2015 BANKNIFTY 17495.45 17353.85 17457.15 17881.95 17032.35 0.0 2015-12-02 09:54:00 0.0 0.0 0.0 0.00 2015-12-02 14:20:00 17185.45 0.0 0.0 0.00 168.40

1 31-12-2015 BANKNIFTY 16972.25 16896.65 16932.50 17159.30 16705.70 2016-01-01 13:41:00 2016-01-01 09:21:00 0.0 2016-01-01 13:41:00 2016-01-01 14:20:00 17046.40 0 0.00 0.0 0.0 74.15 -75.60

2 21-01-2016 NIFTY 7398.70 7250.00 7355.70 7801.80 6909.60 2016-01-22 11:00:00 0 0.0 0 2016-01-22 14:20:00 7421.35 0 0.00 0.0 0.0 22.65 0.00

3 21-01-2016 BANKNIFTY 15364.60 14918.15 15343.15 16682.50 14003.80 2016-01-22 10:01:00 0 0.0 0 2016-01-22 14:20:00 15533.05 0 0.00 0.0 0.0 168.45 0.00

4 15-03-2016 BANKNIFTY 15386.85 15268.10 15304.35 15660.60 14948.10 0 2016-03-16 10:40:00 0.0 0 0 0.00 2016-03-16 14:20:00 15276.65 0.0 0.0 0.00 -8.55

... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ...

166 05-07-2023 NIFTY 19421.60 19339.60 19385.70 19631.70 19139.70 2023-07-06 09:30:00 0 0 0 2023-07-06 14:20:00 19484.50 0 0.00 0 0.0 62.90 0.00

167 10-07-2023 NIFTY 19435.85 19327.10 19427.10 19753.35 19100.85 2023-07-11 09:20:00 0 0 0 2023-07-11 14:20:00 19446.25 0 0.00 0 0.0 10.40 0.00

168 19-07-2023 BANKNIFTY 45707.40 45433.00 45689.05 46512.25 44865.85 2023-07-20 09:23:00 0 0 0 2023-07-20 14:20:00 46126.35 0 0.00 0 0.0 418.95 0.00

169 07-08-2023 BANKNIFTY 45011.35 44773.85 44888.95 45601.45 44176.45 2023-08-08 10:25:00 0 0 0 2023-08-08 14:20:00 44953.35 0 0.00 0 0.0 -58.00 0.00

170 10-08-2023 NIFTY 19623.60 19495.40 19554.25 19938.85 19169.65 0 2023-08-11 09:20:00 0 0 0 0.00 2023-08-11 14:20:00 19471.05 0 0.0 0.00 24.35

171 rows × 19 columns

The backtest is complete. Now, it is time to visualize the data in an easier way. With graphs along with various analytics.

Run Various Performance Metrics

import pandas as pd

# Assuming df is your DataFrame

# Calculate net of buy_pl_points and sell_pl_points

net_buy_pl = df['buy_pl_points'].sum()

net_sell_pl = df['sell_pl_points'].sum()

# Calculate positive, negative, and total occurrences of buy_pl_points

positive_buy_count = (df['buy_pl_points'] > 0).sum()

negative_buy_count = (df['buy_pl_points'] < 0).sum()

total_buy_count = df['buy_pl_points'].count()

# Calculate positive, negative, and total occurrences of sell_pl_points

positive_sell_count = (df['sell_pl_points'] > 0).sum()

negative_sell_count = (df['sell_pl_points'] < 0).sum()

total_sell_count = df['sell_pl_points'].count()

# Print the calculated metrics

print("Net of buy_pl_points:", net_buy_pl)

print("Net of sell_pl_points:", net_sell_pl)

print("Positive buy_pl_points count:", positive_buy_count)

print("Negative buy_pl_points count:", negative_buy_count)

print("Total buy_pl_points count:", total_buy_count)

print("Positive sell_pl_points count:", positive_sell_count)

print("Negative sell_pl_points count:", negative_sell_count)

print("Total sell_pl_points count:", total_sell_count)

This code snippet calculates and analyzes various trading performance metrics from a given DataFrame.

- Net Profit and Loss Calculation: It calculates the net profit (

net_buy_pl) and net loss (net_sell_pl) by summing up all the buy and sell profit/loss points, respectively. - Buy Profit Points Analysis: It computes the count of positive buy profit points (profits) as

positive_buy_count, the count of negative buy profit points (losses) asnegative_buy_count, and the total count of buy profit points astotal_buy_count. - Sell Profit Points Analysis: Similar to the buy analysis, it calculates the count of positive sell profit points (profits) as

positive_sell_count, the count of negative sell profit points (losses) asnegative_sell_count, and the total count of sell profit points astotal_sell_count.

Net of buy_pl_points: 2221.00000000001

Net of sell_pl_points: 4721.430000000011

Positive buy_pl_points count: 46

Negative buy_pl_points count: 27

Total buy_pl_points count: 171

Positive sell_pl_points count: 60

Negative sell_pl_points count: 24

Total sell_pl_points count: 171

Adding the Lot Size

Since the code currently calculates profits in points, it’s essential to incorporate lot size information to determine the quantity. Without specifying the quantity, it becomes challenging to interpret the profit amount and other associated metrics.

However, it’s worth noting that lot sizes can vary over time due to SEBI’s discretion. To address this, we’ll temporarily fix the current lot size within the system and compute profits across the entire dataset while normalizing it. While this approach may be considered unethical for backtesting purposes, the small sample size shouts that the resulting deviation in the output will be negligible and inconsequential.

def calculate_lotsize(row):

if row["symbol"] == "BANKNIFTY":

return 15

elif row["symbol"] == "NIFTY":

return 50

else:

return 40

df["lotsize"] = df.apply(calculate_lotsize, axis=1)

df["buy_pl_points"] = df["buy_pl_points"]*df["lotsize"]

df["sell_pl_points"] = df["sell_pl_points"]*df["lotsize"]

Running More Performance Metrics

Since We have the quantity in place. Let’s get these following metrics –

- Average of all buy_pl_points: This is the average profit or loss for all buy trades.

- Average of all sell_pl_points: This is the average profit or loss for all sell trades.

- Average of positive buy_pl_points: This is the average profit for buy trades that resulted in a profit.

- Average of positive sell_pl_points: This is the average profit for sell trades that resulted in a profit.

- Average of negative buy_pl_points: This is the average loss for buy trades that resulted in a loss.

- Average of negative sell_pl_points: This is the average loss for sell trades that resulted in a loss.

# Assuming df is your DataFrame

# Calculate average of buy_pl_points and sell_pl_points

average_buy_pl = df['buy_pl_points'].mean()

average_sell_pl = df['sell_pl_points'].mean()

# Calculate average of positive buy_pl_points and positive sell_pl_points

average_positive_buy_pl = df.loc[df['buy_pl_points'] > 0, 'buy_pl_points'].mean()

average_positive_sell_pl = df.loc[df['sell_pl_points'] > 0, 'sell_pl_points'].mean()

# Calculate average of negative buy_pl_points and negative sell_pl_points

average_negative_buy_pl = df.loc[df['buy_pl_points'] < 0, 'buy_pl_points'].mean()

average_negative_sell_pl = df.loc[df['sell_pl_points'] < 0, 'sell_pl_points'].mean()

# Print the calculated averages

print("Average of buy_pl_points:", average_buy_pl)

print("Average of sell_pl_points:", average_sell_pl)

print("Average of positive buy_pl_points:", average_positive_buy_pl)

print("Average of positive sell_pl_points:", average_positive_sell_pl)

print("Average of negative buy_pl_points:", average_negative_buy_pl)

print("Average of negative sell_pl_points:", average_negative_sell_pl)

Average of buy_pl_points: 347.5760233918145

Average of sell_pl_points: 563.6125730994178

Average of positive buy_pl_points: 2607.565217391311

Average of positive sell_pl_points: 2375.0291666666717

Average of negative buy_pl_points: -2241.203703703704

Average of negative sell_pl_points: -1921.8333333333273

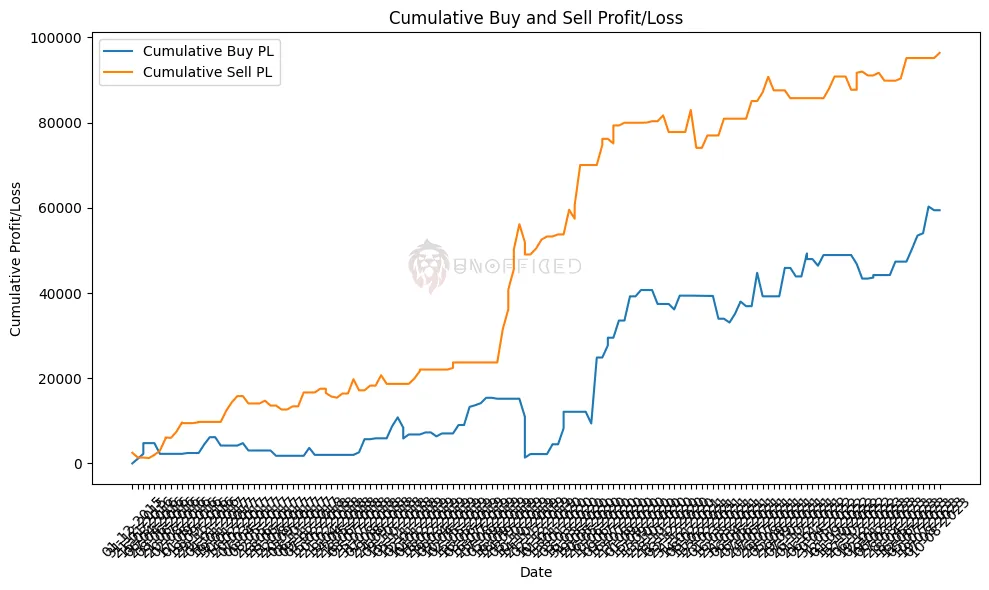

Plotting the Equity Curve

The following code calculates the cumulative profit and loss (PL) over time for both buy and sell trades using the ‘buy_pl_points‘ and ‘sell_pl_points‘ columns in a DataFrame. It creates a line plot that represents the equity curve, also known as the cumulative PL versus time.

In this plot, the x-axis represents time (in this case, dates), and the y-axis represents the cumulative profit or loss. The ‘Cumulative Buy PL‘ line shows the cumulative profit or loss for all buy trades over the given time period, while the ‘Cumulative Sell PL‘ line shows the cumulative profit or loss for all sell trades over the same period.

import pandas as pd

import matplotlib.pyplot as plt

# Assuming df is your DataFrame

# Calculate cumulative sum of buy_pl_points and sell_pl_points

df['cumulative_buy_pl'] = df['buy_pl_points'].cumsum()

df['cumulative_sell_pl'] = df['sell_pl_points'].cumsum()

# Create a line plot

plt.figure(figsize=(10, 6))

plt.plot(df['date'], df['cumulative_buy_pl'], label='Cumulative Buy PL')

plt.plot(df['date'], df['cumulative_sell_pl'], label='Cumulative Sell PL')

plt.xlabel('Date')

plt.ylabel('Cumulative Profit/Loss')

plt.title('Cumulative Buy and Sell Profit/Loss')

plt.legend()

plt.xticks(rotation=45)

plt.tight_layout()

plt.show()

This equity curve provides a visual representation of how the trading strategy has performed over time, allowing you to see trends, fluctuations, and the overall profitability of the strategy.

It helps traders and analysts assess the strategy’s performance and make informed decisions based on historical data.