Nemish Shah’s Investment Strategy

He manages thousands of crores, co-founded one of India’s most powerful investment banks, and appears on no magazine cover. Meet the investor Dalal Street quietly calls “India’s Charlie Munger” — and who calls himself nothing at all.

The Invisible Billionaire

Open any list of India’s top ten individual shareholders by market value. Rakesh Jhunjhunwala is there. Radhakishan Damani is there. Dolly Khanna, Vijay Kedia, Ashish Kacholia — all present, all photographed, all endlessly quoted.

And then, somewhere in the middle of that list, sits a name most retail investors cannot pick out of a line-up: Nemish S. Shah.

No interviews. No Twitter. No channel appearances. No book tour. Just a Mumbai address, a famously minimalist office, and a public shareholding worth thousands of crores in a handful of companies he has owned — in several cases — for more than two decades. When Axis Bank took over ENAM’s banking and broking business, he did not show up to a single press conference.

“If you cannot describe a business on the back of a napkin, you do not understand it well enough to own it.” — Nemish Shah, attributed

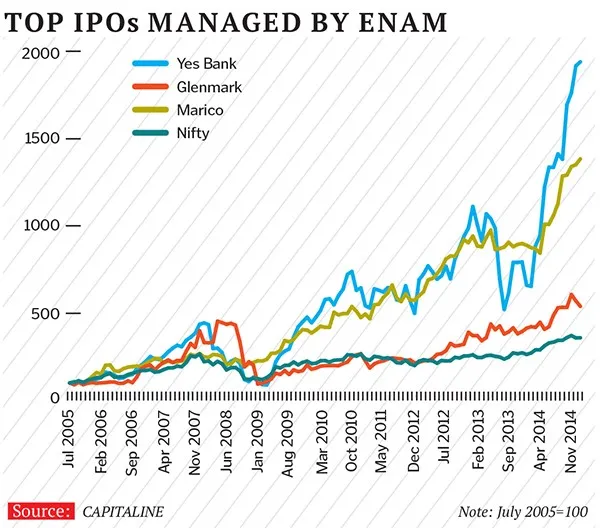

ENAM: A Firm Built Out of Four Surnames

In the early 1980s, four young men in Bombay pooled their initials and their savings and set up a broking firm. They called it ENAM — a name assembled from their surnames. By the 1990s, ENAM had become one of the most respected investment banks in India, run primarily by Vallabh Bhansali and Nemish Shah.

The division of labour was famous inside the firm. Bhansali was the face — the orator, the man who met promoters and presided over IPOs. Shah sat quietly in his room, reading annual reports and managing the proprietary book. That proprietary book would become one of the most successful equity portfolios in Indian history.

In 2012, Axis Bank acquired ENAM’s investment banking operations. Shah stayed back to run the treasury operations at ENAM Holdings Pvt. Ltd., where he continues to compound capital away from the spotlight. The focus of his portfolio has never changed: long-term investing in Indian equity.

He employs a fundamental bottoms-up research approach to identify high-quality businesses that are structurally well-positioned, have sustainable competitive advantages, and executional ability for consistent long-term growth.

In fewer words — he is a value investor. But how does he actually apply value investing in the Indian market?

Nemish Shah’s Investment Strategy

Rule #1 — Management First, Business Second, Price Third

After years of refusing interviews, Shah finally opened up briefly to Forbes India. His message was blunt: in India, the only crucial difference from investing in the rest of the world is that you must look at the quality of management very closely.

As long as the management is focused and understands allocation of capital, Shah is comfortable with the business. He has ignored many names simply because the promoter didn’t give him “the right vibe” — he has refused to buy businesses on spreadsheet merit alone. This is how he picked up Asahi India Glass at a deeply undervalued price long before the market caught up with it.

Rule #2 — ROCE Below 9% = Wealth Destruction

- If the return on capital employed (ROCE) numbers are less than nine percent, the company is a wealth destroyer. What is the point of being in the business if you can’t generate a sustainable ROCE?

- Shah also dislikes cases where promoters are constantly raising fresh capital and diluting equity. What matters most to him is how the funds for future growth are planned — ideally out of internal accruals, on a clear timeline, rather than opportunistic placements.

Consider the infrastructure sector. Promoters borrowed heavily on the back of optimistic traffic projections, low interest rates, and assumptions of quick project completion. In effect, they left themselves almost no room for error.

If any of the projections went wrong, the company would have a hard time paying off its debt. Shah concedes that companies in such sectors may suffer from external shocks — but he believes that with good management, a company can find a way to survive and grow even under stress.

Take commodity companies like JSPL (Jindal Steel & Power Limited). The stock was available for ₹2 in 2001. Over the following fifteen years, it compounded at ~37% annually against the index’s 15%. Shah attributes almost the entire outsized return to Naveen Jindal’s execution — captive coal, captive power, backward integration and relentless capital discipline. “Great management,” he has said, “can turn even a commodity into a compounder.”

Infosys and Yes Bank: Backing the Promoter, Not the Model

Until the 1990s, Indian companies were not obliged to report earnings more than once a year. Analysts mostly questioned dealers, distributors and customers to piece together the picture. In 1993, Infosys changed that. It began declaring half-yearly results, then quarterly. Regulators eventually made it mandatory for everyone.

Guess who managed the Infosys IPO and the Yes Bank IPO? ENAM.

Shah worked extraordinarily hard to ensure the Infosys issue did not go under-subscribed. He has since admitted that at the time he did not believe a Bangalore software exporter could become a global giant — but he believed in N. R. Narayana Murthy’s management. His team had to convince investor after investor to come in.

A few years later, the dot-com boom swept through and flushed out most Indian IT companies. Infosys survived. Shah credits the survival, and the subsequent compounding, entirely to management quality. When the stock fell 70–80% in 2000, he didn’t sell. He added.

E-commerce and the Problem of Non-Linear Growth

Shah sees a familiar kind of valuation madness in today’s e-commerce businesses.

Unlike conventional businesses, where growth patterns are linear, e-commerce does not have a straight-line growth path. In that context, it is very difficult to challenge these companies on their potential numbers over the next few years.

Because those staggering numbers cannot be reliably discounted to a present value, investors end up paying almost any valuation for them. Shah, however, does not think the sector is yet in bubble territory — the potential size is so vast that “we may not even have wrapped ourselves around the true potential of the business.”

The Three Questions Shah Asks

The Three Questions Shah Asks

- Size of the opportunity. How big is the pond? Even a great fisherman catches little in a small one.

- Quality of the management. In a non-linear business, the driver matters more than the car.

- Entry price. A wonderful business bought at a terrible price is still a terrible investment.

Shah refuses to invest in tobacco, hotels and liquor — not for valuation reasons, but because they don’t fit his personal philosophy. When asked to recommend a single book that reflects his approach, he pointed to only one title: Berkshire Hathaway Letters to Shareholders. “Everything I believe about investing,” he has said, “Buffett and Munger said first, and said better.”

What Retail Investors Can Steal From Him

- Own fewer, know them deeper. Shah’s real edge isn’t information — it’s familiarity. He owns businesses he has tracked for twenty years.

- Let the ROCE filter do the rejecting. Most “opportunities” quietly destroy wealth. A hard ROCE minimum saves you from most of them.

- Judge the promoter before the P&L. In India especially, numbers are authored. Find out who the author is.

- Say no to entire categories. Shah’s tobacco/hotels/liquor exclusion has cost him some returns. It has also kept him intellectually honest for decades.

- Absence is a position. Not owning something risky is often the best trade you didn’t make.

In a market addicted to noise, Nemish Shah’s career is a quiet argument for its opposite — that the best investors are often the ones you have never heard speak.

[…] Strategy Earn 86% per year with ShopKeeper Startegy How to use Candlestick Charting to make money Nemish Shah’s Investment Strategy How to find Undervalued Stocks in Indian Share Market How do I perform market sector analysis […]