import math

from scipy.stats import norm

def black_scholes_dexter(S0,X,t,σ="",r=10,q=0.0,td=365):

if(σ==""):σ =indiavix()

S0,X,σ,r,q,t = float(S0),float(X),float(σ/100),float(r/100),float(q/100),float(t/td)

#https://unofficed.com/black-scholes-model-options-calculator-google-sheet/

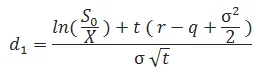

d1 = (math.log(S0/X)+(r-q+0.5*σ**2)*t)/(σ*math.sqrt(t))

#stackoverflow.com/questions/34258537/python-typeerror-unsupported-operand-types-for-float-and-int

#stackoverflow.com/questions/809362/how-to-calculate-cumulative-normal-distribution

Nd1 = (math.exp((-d1**2)/2))/math.sqrt(2*math.pi)

d2 = d1-σ*math.sqrt(t)

Nd2 = norm.cdf(d2)

call_theta =(-((S0*σ*math.exp(-q*t))/(2*math.sqrt(t))*(1/(math.sqrt(2*math.pi)))*math.exp(-(d1*d1)/2))-(r*X*math.exp(-r*t)*norm.cdf(d2))+(q*math.exp(-q*t)*S0*norm.cdf(d1)))/td

put_theta =(-((S0*σ*math.exp(-q*t))/(2*math.sqrt(t))*(1/(math.sqrt(2*math.pi)))*math.exp(-(d1*d1)/2))+(r*X*math.exp(-r*t)*norm.cdf(-d2))-(q*math.exp(-q*t)*S0*norm.cdf(-d1)))/td

call_premium =math.exp(-q*t)*S0*norm.cdf(d1)-X*math.exp(-r*t)*norm.cdf(d1-σ*math.sqrt(t))

put_premium =X*math.exp(-r*t)*norm.cdf(-d2)-math.exp(-q*t)*S0*norm.cdf(-d1)

call_delta =math.exp(-q*t)*norm.cdf(d1)

put_delta =math.exp(-q*t)*(norm.cdf(d1)-1)

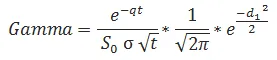

gamma =(math.exp(-r*t)/(S0*σ*math.sqrt(t)))*(1/(math.sqrt(2*math.pi)))*math.exp(-(d1*d1)/2)

vega = ((1/100)*S0*math.exp(-r*t)*math.sqrt(t))*(1/(math.sqrt(2*math.pi))*math.exp(-(d1*d1)/2))

call_rho =(1/100)*X*t*math.exp(-r*t)*norm.cdf(d2)

put_rho =(-1/100)*X*t*math.exp(-r*t)*norm.cdf(-d2)

return call_theta,put_theta,call_premium,put_premium,call_delta,put_delta,gamma,vega,call_rho,put_rho

The function to find the option price using Black-Sholes model refers to indiavix() function but the function’s definition is not found in the code. Where can I find the indiavix() function?

Check the library used.